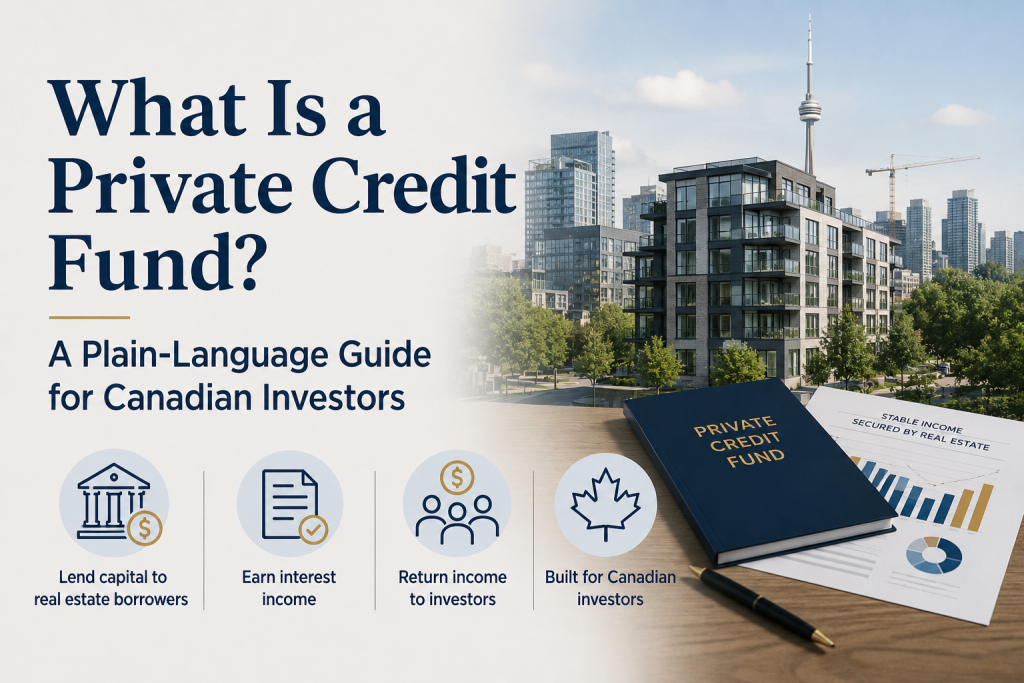

What Is a Private Credit Fund? A Plain-Language Guide for Canadian Investors

The term “private credit” has moved from institutional investment jargon into the mainstream vocabulary of accredited investors across Canada — and for good reason. As interest rates have reset higher and traditional fixed income has struggled to keep pace with inflation, private credit has emerged as a compelling income-generating alternative for sophisticated investors.

But what exactly is a private credit fund, and how does one evaluate the options available in the Canadian market?

Private Credit: The Basic Concept

Private credit refers to loans made by non-bank lenders — typically funds or investment vehicles — to borrowers who need capital outside the conventional banking system. In the real estate context, these are typically mortgage loans secured against commercial, industrial, or development properties.

The lending process works like this: a real estate developer, property owner, or builder needs capital that a traditional bank either won’t provide (due to lending criteria) or can’t provide quickly enough (due to approval timelines). A private credit fund steps in, underwrites the loan, and provides the capital — charging an interest rate that reflects the risk profile of the loan.

That interest income, along with any fees charged to the borrower, is then distributed to the fund’s investors — typically on a monthly or quarterly basis.

How Is This Different from a Mortgage Investment Corporation (MIC)?

A Mortgage Investment Corporation (MIC) is a specific Canadian corporate structure that also invests in mortgages and distributes income to shareholders. A private credit fund structured as a Limited Partnership (LP) or Mutual Fund Trust is a different legal vehicle, though the economic model — lending capital and distributing interest income — is similar.

The key differences lie in the tax treatment of distributions, the fee structure, the management approach, and the investor eligibility criteria. LP-structured private credit funds can offer tax treatment advantages for certain investors, particularly corporations — a feature explored in more detail in our article on tax treatment.

What Makes a Strong Private Credit Fund?

Not all private credit funds carry the same risk profile or investor alignment. Sophisticated investors evaluate these vehicles across several dimensions:

Loan Security: Are loans secured by real property? What is the loan-to-value ratio? Lower LTV means more borrower equity between the loan and the property value — providing a cushion in enforcement scenarios.

Loan Position: First mortgage positions are senior to all other claims on the property. Second mortgage positions carry more risk but also earn higher rates. A well-structured fund balances these positions thoughtfully.

Underwriting Discipline: How does the fund evaluate borrowers? What criteria govern loan approval? A fund with rigorous underwriting standards will have a materially better loss track record than one that prioritizes volume over quality.

Fee Structure: Where do origination, renewal, and administration fees go — to the manager or to investors? A fund that routes all fee income to investors is structurally more aligned than one that allows the manager to extract fees at the borrower level.

Track Record: How long has the manager been lending? What is the historical loan loss rate? A demonstrated track record of conservative underwriting and low losses is a leading indicator of future performance.

Distribution Frequency: Monthly distributions are preferred by income-focused investors. Quarterly or annual distributions require investors to wait longer to access their return.

Registered Account Eligibility: Can the investment be made inside an RRSP, TFSA, or other registered account? This significantly affects after-tax yield for many Canadian investors.

The Evertrust Private Credit Fund: Applying the Framework

The Evertrust Private Credit Fund LP addresses each of these criteria thoughtfully. It lends primarily in first mortgage positions (70%), targets LTVs of 50–65%, employs rigorous institutional-grade underwriting, routes all fee income to investors rather than the manager, distributes income monthly, and is eligible for registered accounts including RRSP, TFSA, RESP, RRIF, and LIRA.

The fund is backed by a management team with a decade-long track record of mortgage lending on over $280 million of funded mortgages — with an average annual loan loss rate of just 23 basis points.

The targeted annual net return is 9% for Class A Units, with monthly distributions.

Book an appointment online: Read More

Visit: https://www.frontfundr.com/evertrust

Call: 647-501-2345 ext. 112 Email: info@evertrustdevelopments.com

This article is for informational purposes only. Please review all offering documents and consult your financial advisor before investing.