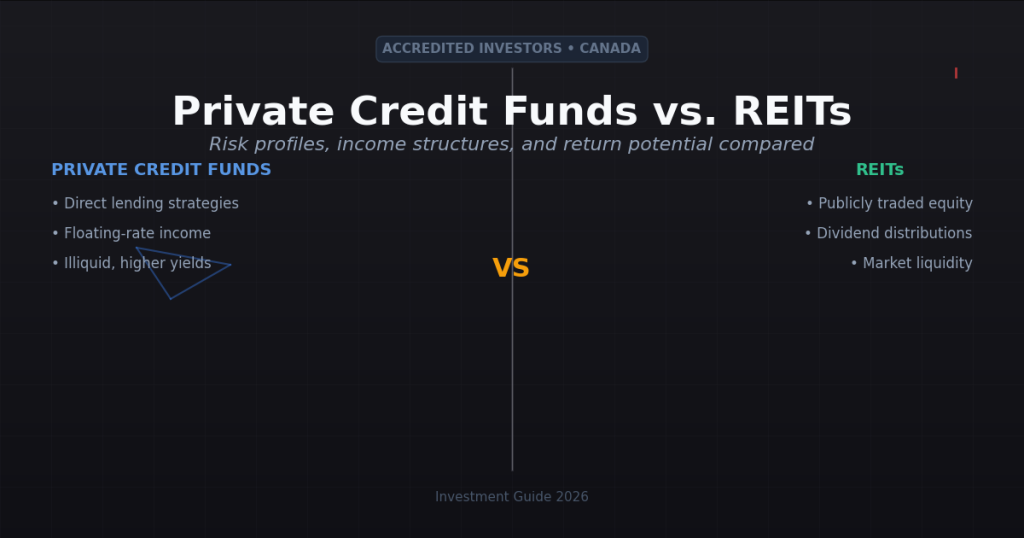

Private Credit Funds vs. REITs: What Accredited Investors in Canada Need to Know

For investors seeking real estate exposure in their portfolio, two of the most frequently discussed options are publicly traded Real Estate Investment Trusts (REITs) and private credit funds secured by real estate assets. Both are real estate-related. Both generate income. But they operate very differently — and the distinction matters for accredited investors who are building an income-oriented portfolio.

What REITs Are and How They Work

A publicly traded REIT owns and operates a portfolio of income-producing real estate assets — shopping centres, office buildings, industrial warehouses, apartment buildings, or some combination thereof. REITs are listed on public stock exchanges, trade daily, and distribute at least 90% of their taxable income to unitholders.

REITs offer accessibility and liquidity: investors can buy and sell units any time markets are open, and they can invest through registered accounts with relatively low minimums.

But REITs also carry the characteristics of publicly traded securities: their unit prices fluctuate with equity market sentiment, interest rate expectations, and sector-specific news — sometimes sharply and without relation to the underlying performance of the real estate the REIT owns. A REIT’s yield may be 5% on fundamentals while its unit price falls 20% in a market correction, generating a net negative total return despite the income.

What Private Credit Funds Offer

A private credit fund secured by real estate operates differently. It does not own real estate — it lends to real estate operators and earns interest on those loans. This distinction changes the risk and return profile materially:

No public market correlation: Private credit funds are not traded on exchanges. Their valuations are tied to the performance of the underlying loan portfolio — not to equity market sentiment or interest rate speculation. A market correction does not cause the fund’s value to drop unless loans in the portfolio actually default.

Contractual income: Interest payments from borrowers are contractual obligations, not discretionary distributions. As long as borrowers are current on their loans, investors receive their distributions. REIT distributions, by contrast, can be reduced or suspended at management’s discretion.

Capital stack seniority: A first mortgage lender is senior to all equity in the capital structure. A REIT unitholder is, economically, an equity investor — they own a share of the residual value after all debt is paid. In a downturn, debt holders recover before equity holders.

Higher yield potential: Private credit funds targeting 9% net annual returns exceed the current distribution yield of most Canadian REITs, which typically range from 4–6%.

The Trade-Offs: What REITs Offer That Private Credit Doesn’t

REITs are more accessible (no accredited investor requirement), more liquid (daily trading), and more transparent (public disclosure requirements). They can be held with no minimum investment and are available to all Canadian investors.

Private credit funds require accredited investor status, a minimum subscription ($100,000 for the EPCF), and a longer-term commitment horizon. They are less liquid and carry the complexity of private placement investments.

For accredited investors who meet the eligibility criteria and have adequate liquidity elsewhere in their portfolio, the trade-off between REIT liquidity and private credit yield and structural seniority often favours private credit for the income allocation of a diversified portfolio.

The Evertrust Private Credit Fund as a REIT Alternative

For accredited investors evaluating real estate income exposure, the Evertrust Private Credit Fund LP offers:

- 9% targeted annual net return vs. 4–6% typical REIT yield

- Monthly distributions with no public market price volatility

- First mortgage security on underlying real estate assets

- Registered account eligible (RRSP, TFSA, RESP, RRIF, LIRA)

- Business income tax treatment for corporate investors

- $25,000 minimum for accredited investors

Call: 647-501-2345 ext 112 Email: info@evertrustdevelopments.com

This article is for informational purposes only. REITs and private credit funds carry different risk profiles. Please consult your advisor before investing.